When it comes to compensation philosophy, your equity comp “percentile philosophy” moves the needle substantially more than your cash comp philosophy.

Let’s explore this concept, and look at some sample benchmarks to illustrate the point.

The Varying Compensation Philosophies on Percentiles

“What percentile of the market do you pay at?” I ask a lot of companies this question, and three things surprise about the responses.

1. I seldom hear a customer explicitly say a number that is less than the 50th percentile. Yet mathematically, half of the market has to pay below the 50th percentile.

2. Companies generally fall into one of four buckets, and it’s usually tricky to identify which bucket they are in without a few more follow-up questions:

- The company picks a single percentile that applies to both cash and equity.

- Two percentiles: one for cash, and one for equity.

- A percentile that only applies for cash. And for equity, things are a bit more hand wave-y.

- No percentiles at all. Just “we use market data to inform our ranges”, and that’s it.

3. I ask if companies share their percentile philosophy with candidates and employees. The answer is usually “no” across the board, sometimes yes for cash, and seldom yes for both cash and equity.

This begs the question—what is the importance of a definitive percentile for your cash ranges vs the importance of a definitive percentile for your equity targets/guidelines/ranges?

{{mid-cta}}

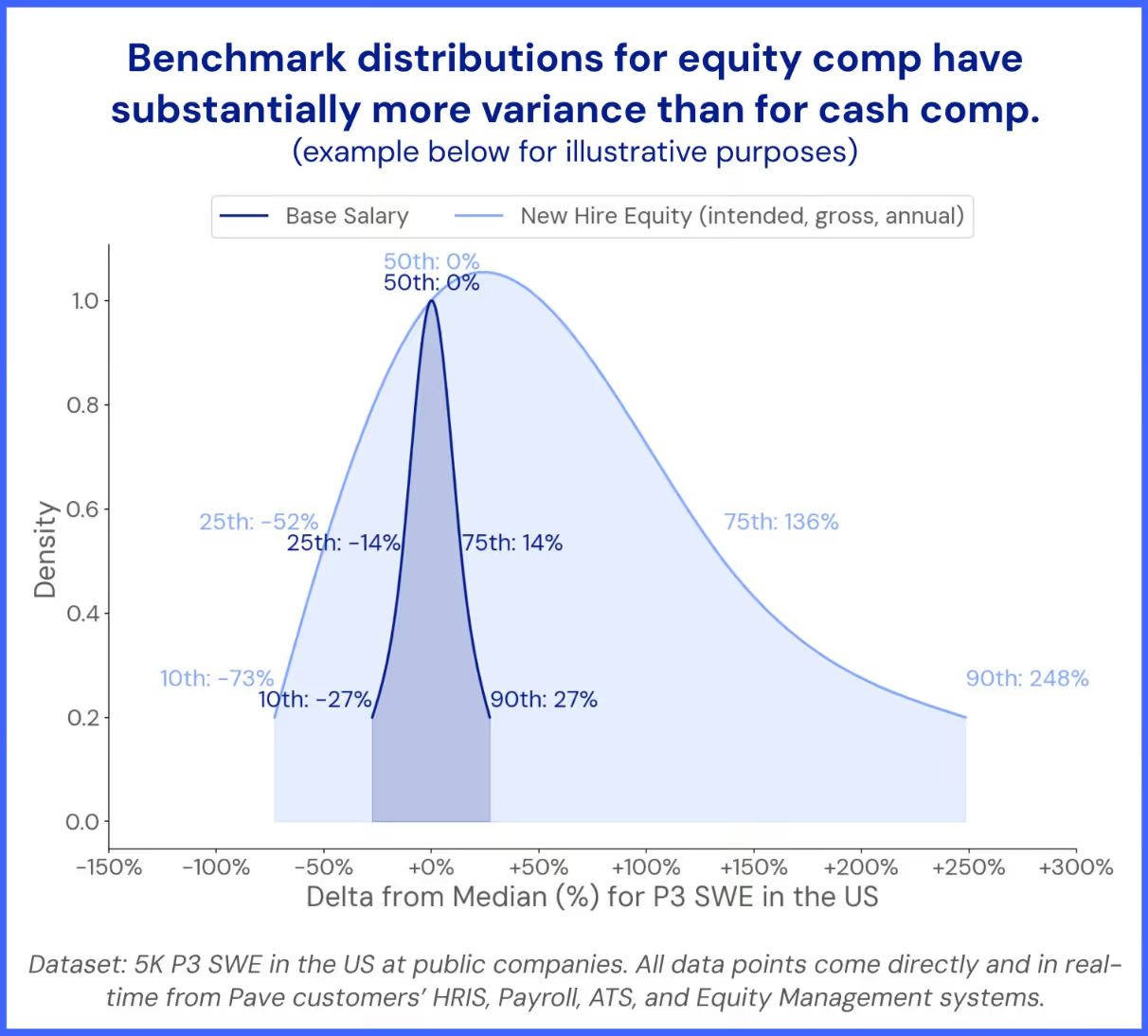

Cash vs Equity Compensation Distribution

Turns out, the benchmark distributions look very different for cash vs equity distributions. We analyzed P3 SWEs at public tech companies within Pave’s dataset to illustrate an example of how equity comp has substantially more variance than cash compensation.

From this, we can see that, in general:

- Equity distributions are much wider than cash distributions.

- Equity distributions are more right-skewed than cash distributions. The top outliers are paid disproportionately more in equity comp.

The equity compensation philosophy you decide on potentially carries substantially more weight than your cash compensation philosophy. Stock-based compensation is not "free lunch".

What does your company do to set its cash and equity compensation guidelines?

.avif)

Matt Schulman is CEO and founder of Pave, the complete platform for Total Rewards professionals. Prior to Pave, he was a software engineer at Facebook focusing on user-centric mobile experiences. A self-proclaimed "comp nerd," Matt is known for sharing data-driven thought leadership around all things compensation and personal finance.